Accounting Ethics, Professional Identity, and the Public Interest

While accounting remains one of the most trusted and respected of all professions, the industry has been roiled by several high-profile ethics scandals of late. In 2019, the Securities Exchange Commission (SEC) levied a $50 million penalty against accounting firm KPMG for possession of stolen Public Company Accounting Oversight Board (PCAOB) inspection information and for evidence that employees were cheating on internal ethics exams. In 2022, the SEC fined accounting firm Ernst & Young (EY) $100 million – the largest penalty against an accounting firm by the SEC in history – for cheating on the Certified Public Accountant (CPA) ethics exam and for withholding evidence from investigators. The CEO of PriceWaterhouse Coopers PWC Australia resigned in 2023 after an investigation revealed that confidential government tax plans had been shared within the firm. Accounting firms have also been criticized for their failure to detect financial frauds at their clients in recent years, including EY (Wirecard) and Deloitte (Go-Ahead). In September 2025, a U.S. Senate investigation found that KPMG had ignored red flags and risks that led to the collapse of Silicon Valley Bank, Signature Bank, and First Republic Bank, with Senator Richard Blumenthal boldly proclaiming, “This industry is a joke.”

News of these shocking scandals begs the question, has accounting lost its moral high ground? The answer to this question holds importance for accounting, but also for society more broadly. We often take it for granted, but the very foundations of commerce depend upon having reliable financial information. Corporations access the capital they need to innovate, produce, serve, trade, hire, and grow, because investors have faith in the quality of the companies’ financial reporting. Without reliable financial reporting to inform decision making, the cost of doing business would rise as trading and investing partners would have to price in increased information risk. In an environment without reliable financial reporting, businesses would find it harder to compete and the economy would contract. If we stop trusting the accountants, how long before we lose trust in financial reporting, business, and the financial markets as a whole?

In short, we need comprehensive solutions to the accounting ethics problem to protect the public interest. These solutions must involve strong support and consistent messaging from leaders. Structural impediments to ethical decision making, especially conflicts of interest and ambiguity around the importance of compliance practices, need to be resolved. Indeed, both EY and KPMG have been ordered by the SEC to bring in outside consultants to review their policies and procedures relating to ethics and integrity.

However, the work cannot stop there. What the recent ethical lapses bring into sharp focus is the fact that a significant number of accountants knowingly ignored the values that the accounting profession has historically been known for – values like integrity, honesty, self-sacrifice, and protecting the public interest. We must seek to understand how so many accountants rationalized cheating on an ethics exam, withholding evidence from investigators, or sharing confidential information as acceptable choices. We need to bring attention to aspects of accounting culture that may have implicitly contributed to the rationalization of this unethical behavior in the first place.

If we view the recent accounting ethics scandals through the lens of the professional identity, it suggests that the problem may be traced to a simmering existential crisis in the field rather than just a result of conflicts of interest, bad training, weak policies, or some other structural impediment to ethical decision making. An accountant who identifies strongly with the principles and values of the profession would never cheat or lie or share confidential information, because doing so would go against the very core of who they define themselves to be. Such behavior would constitute a violation of selfhood that would be unconscionable.

Is it possible that significant numbers of accountants have lost their sense of pride in their work and as a result, become disconnected from the principles and values of the profession? Anecdotal evidence suggests a recent uptick in concern about the profession’s identity. For instance, a 2022 Wall Street Journal headline reads, “Why So Many Accountants Are Quitting: Even Some Accounting Majors Don’t Want Accounting Jobs,” Moreover, the American Institute of Certified Public Accountants (AICPA) has recently been engaged in efforts to “reboot” the profession’s image, acknowledging the problems of both declining enrollments in accounting programs and high turnover within the profession.

This article explores the concept of professional identity, how it informs ethical decision making, and concludes with five strategies that may help the accountants rebuild the public’s trust in their abilities to conduct themselves with integrity.

Ethics and Professional Identity

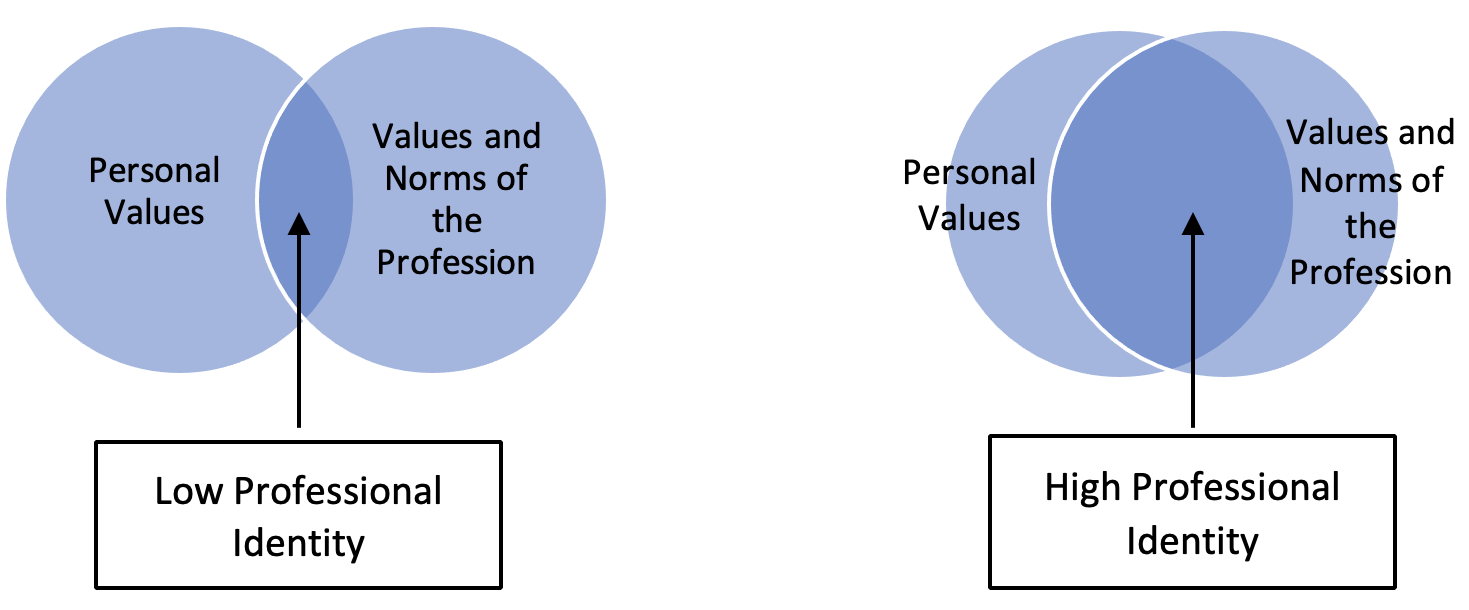

Professional identity is a concept that captures the extent of the overlap between an individual’s personal values and the values and norms of their chosen profession. Studies across a range of professions – engineering, health care, law, teaching, social work, and accounting – show that when the overlap between personal and professional value systems is high, the decision maker is likely to make choices that align with and benefit the professional group. Research suggests that practitioners with a strong sense of professional identity behave more ethically, because they have internalized their profession’s core values. This internalization of core values produces a resilient moral compass that fosters the moral courage necessary to uphold these values even in difficult situations.

Figure 1. Professional Identity

Examining the accounting profession specifically, research shows that an auditor with a strong sense of professional identity is more likely to demonstrate professional skepticism and resist client pressure to accept an aggressive accounting treatment. Professional identity has also been shown to increase motivation and performance on auditing tasks. Importantly, many studies have linked having a strong professional identity or professional commitment to ethical behavior among accountants. On the other hand, when professional identity or professional commitment is weak, decision makers will generally work to their own benefit. One qualitative study of accountants also identified weak professional identity as the primary cause of cynicism and resistance to rules and regulations in auditing.

Thinking about ethics, independence, and objectivity from the perspective of professional identity highlights important factors in ethical decision making, like the sense of self and feelings of belonging, which often get ignored when we think about ethics as simply a problem of mis-aligned incentives. Examining accounting ethics as an identity problem suggests that the way forward should go beyond ethics and compliance training to also explore the existential questions that may have contributed to the current problem. If we can strengthen accountants’ sense of professional identity, we can help them feel less conflicted about their role responsibilities and more empowered to make ethical choices.

Strategies for Strengthening Professional Identity

Dispelling Myths About the Profession. We can begin our efforts to strengthen professional identity by dispelling myths about the profession. Surveys of student attitudes towards the accounting profession frequently identify several misconceptions about accounting that may be standing in the way of attracting people to the profession who share its values. Accountants are often negatively stereotyped in the media, so it is not surprising that many people mistakenly view accounting as a boring, solitary profession populated by “bean counters” rather than team players. In fact, accountants do most of their work in a team environment. Experienced auditors will tell you that the social skills of being able to work well with others and develop a healthy relationship with the client are essential to success. The profession also offers unique opportunities to engage in complex thinking, to develop leadership skills, and to demonstrate responsibility early in one’s career.

While the The American Institute of Certified Public Accountants (AICPA) and other accounting organizations may have primary responsibility for helping to combat the image problem facing the profession, their efforts would be greatly amplified if more practicing accountants made time to visit schools and educate young people about accounting careers and the profession’s importance to the efficient functioning of our markets. Giving students the chance to meet a practicing accountant and learn first-hand about the opportunities the profession holds for them would help break down old stereotypes about accounting and provide a point of inspiration and pride for future workers.

Making the Public Interest More Salient. Another way that we can restore a strong, positive professional identity for accountants is to make the public interest responsibility of the profession more salient to new and existing professionals. The responsibilities principle of the AICPA professional code of conduct emphasizes the importance of the accountant’s duty to serve the “public interest.” It reminds accountants that they perform an essential role in society, so they have a continuing responsibility to “cooperate with each other to improve the art of accounting, maintain the public’s confidence, and carry out the professional’s special responsibilities for self-governance.” The public interest principle also encourages accounts to “accept the obligation to act in a way that will serve the public interest, honor the public trust, and demonstrate a commitment to professionalism.” Moreover, the integrity principle sets forth that integrity is the most important character trait of an accountant and the “benchmark against which a member must ultimately test all decisions.” The integrity principle demands that the accountant be “honest and candid” (within the constraints of client confidentiality) and to place service and duty to the public trust above personal gain an advantage.

Reinforcing the public interest aspect of the profession and keeping the importance of public duty front of mind can be difficult when the concepts themselves are both abstract and distant. To help make these concepts more tangible and salient, accountants can make it a habit to take the perspective of a typical “main street investor,” like a teacher with their savings invested in a retirement fund, when trying to determine if a particular accounting choice is appropriate. Trying to view decisions through the eyes of a specific representative of the interested public – that is, putting names and faces to the otherwise amorphous concept of public interest – not only makes the responsibility principle more tangible, but also brings in a sense of emotional connection (empathy) that is an important element of ethical decision making.

Another way to help accountants feel more connected to the public interest is through volunteering in the community through programs like Volunteer Income Tax Assistance (VITA). In this program, accountants help to prepare tax returns for low-income filers, and in doing so, they can see the positive impact of their work on society. Through direct service, an abstract concept like “the public interest” becomes much more tangible.

Accountants can also make the public interest more salient by engaging in reflective exercises that encourage them to think deeply about the principles at the core of the profession. For instance, one study shows that the experimenter was able to significantly increase participants’ positive feelings about their professional identity simply by having them complete a mind mapping exercise that brought their attention to the values of the accounting profession. Self-reflection is a central component of the “Giving Voice to Values” ethics training program used across many corporations today, and research shows that it can have a positive effect on learning accounting ethics, as well.

Strengthening Group Norms. Another strategy for strengthening professional identity is to start small and work at the team level. Research has shown that being a part of a team with strong group norms motives auditors to focus on the greater goal of conducting high quality audits. We also know that having strong mentors and role models helps employees appreciate the long-term benefits of an accounting career. In addition, fostering psychological safety on teams can help employees feel a stronger sense of belonging and acceptance, which may also help them embrace their identities as accountants.

Fraud Awareness. Without a strong sensitivity to fraud risks, it can be hard to appreciate the critical role that accounting plays in the efficient functioning of our markets, an aspect of professional identity that should be a source of pride for accountants. Today’s staff accountants missed growing up in the era of the large financial scandals like Enron or WorldCom, so the concepts of fraud, risk, and audit failure are understandably less salient for Generation Z. Moreover, the likelihood that they will identify misstatements, whether due to fraud or error, are lower than ever thanks to regulatory reforms, better control environments, and advances in technology. Unfortunately, this improvement in financial reporting quality may have an overlooked downside. Without frequent exposure to misstatements, it may be difficult for today’s accountants to see the importance of procedures designed to improve financial reporting quality and protect the public interest.

Research suggests that we can change these sentiments and build appreciation for the importance of auditing and compliance by increasing fraud awareness. In fact, a recent study shows that high school students who were exposed to news about a fraud in their formative years were more likely to major in accounting and to be stronger performers in their auditing careers. For those already working in the profession, we can build greater fraud awareness by sharing case studies about fraudulent activities and keeping abreast of trends in fraudulent activity across industries and around the globe by studying the reporting of organizations like the Association of Certified Fraud Examiners. Partners and directors can also encourage greater fraud awareness and professional skepticism in their teams by telling stories about their personal experiences of finding frauds and misstatements, by bringing attention to potentially suspicious findings or patterns of behavior, and by role modeling appropriately skeptical behavior.

Mitigating Burnout. Finally, we need to appreciate that it is hard to feel connected to one’s profession when the workload becomes overwhelming and gets in the way of living a meaningful life. Even before the reprioritization of work-life balance that many workers experienced during the pandemic, public accounting firms were experimenting with ways to minimize burnout among their employees so that they could increase worker retention and engagement. Most firms now offer employees flexible schedules and opportunities to work remotely, which has greatly improved employee job satisfaction levels. Some firms also offer sabbaticals as a way for top performing employees to make time for self-reflection, personal well-being, and planning for the future. Other firms have encouraged employees to think about their careers more as lattices than ladders by allowing employees to make lateral moves or to reduce their hours when they need to care for children, aging parents, or themselves. In short, there appears to be a new emphasis on addressing the causes of stress and burnout among accounting professionals. If we continue to foster programs and practices that mitigate burnout, we should see improvements in employees’ sense of professional identity and professional commitment.

Conclusion

The recent ethics scandals in prominent public accounting firms threaten to undermine the credibility and reputation of the accounting profession and to destabilize the financial markets as a whole. While conflicts of interest, pressures, weak policies and other compliance breakdowns undoubtedly played a role in these ethical failures, we also need to understand how a significant number of good people were able to rationalize making such obviously bad choices. Professional identity research suggests that choosing a career where the values and norms of the profession align with our own supports ethical decision making. We should be proud of what we do for a living and the role our work plays in society. We need strong leaders who are not afraid to talk about their values and model the importance of ethics in the accounting profession. As we seek to rebuild public trust in the accounting profession, we should also seek to rebuild pride among accountants. Indeed, having a strong professional identity to complement the reforms already underway may be just the missing ingredient needed to help the accounting profession regain the moral high ground and restore trust in the financial systems that our society depends on.

References are attached.

About the Author:

Professor Megan Hess joined the Williams School of Commerce, Economics, and Politics at Washington and Lee University after completing her doctorate in business administration at the Darden Graduate School of Business at the University of Virginia in 2013. She teaches courses in accounting, ethics, and corporate sustainability. Prior to beginning her doctoral studies, she spent twelve years in industry, most recently with Deloitte, where she investigated financial statement fraud. She also holds an MBA from Texas A&M University and a BA from Washington and Lee University. Professor Hess’s research explores the intersection of ethics and accounting, with a focus on topics such as fraud risk management, ethical leadership, whistle-blowing, and sustainability accounting. She has presented her work at numerous academic conferences, published in both management and accounting journals, and authored award-winning teaching cases.